A Year in Review and Expectations for 2026

Posted by Knight Frank Newcastle on 12th December 2025 -

As 2025 draws to a close, it’s fair to say the residential development sector has faced the most challenging year in recent memory. Higher borrowing costs, regulatory hurdles, and subdued buyer confidence have weighed heavily on activity, leaving many developers navigating a complex and uncertain landscape. Yet, despite these headwinds, there are signs of resilience and opportunity emerging.

Looking ahead to 2026, the outlook is cautiously optimistic. On paper, a combination of lower interest rates, planning reform, and renewed confidence should unlock momentum. In this edition, we take stock of the past year and explore where the next 12 months might offer a brighter path for landowners, developers, and investors alike.

For a deep dive on the outlook for the Living Sectors in the coming 12 months, covering build to rent, student property and senior living, I recommend signing up to Capital Clarity, our new quarterly update by Katie O’Neill.

UK Residential Development

Year in review: Major housebuilders dominated land acquisitions in 2025, though demand was highly selective, focused on sites aligned with regional strategies. This has shaped pricing: well-located, consented sites attracted strong competition, but overall values have softened. Knight Frank’s Development Land Index shows greenfield and urban brownfield prices fell 5% annually to Q3 2025. Urban land demand in key regional cities remains muted amid viability pressures. Sales conditions improved compared with last year but remain challenging, particularly in lieu of some form of government incentive for first-time buyers. While sales rates have risen from post-Covid lows, they sit below long-term norms, and the continued use of incentives signals ongoing pressure in pricing and buyer confidence.

Expectations for 2026: Government priorities around housebuilding and planning reform will keep strategic land in focus. Grey belt sites on the edge of conurbations, with strong transport links and clear local demand, are likely to see heightened interest. If base rate cuts continue as forecast, confidence among consumers and developers should strengthen, driving demand for land and new homes. This will likely coincide with improved site supply as NPPF reforms bed in, supporting greater activity across the market. Grant funding will be key to unlocking delivery. Bulk sales and forward funding will remain key tools for managing risk and liquidity (institutions spent more than £1 billion funding single family housing for rent between Q1 and Q3 2025, largely through deals with housebuilders), though typically at a discount. These underscore the ongoing challenge of slower private sales despite improving conditions.

London Development Land

Year in review: The challenges facing London’s development sector persisted throughout 2025. While a slight easing in debt costs offered some relief, slower sales rates, rising build costs, and regulatory delays - such as Gateway 2 - continued to weigh on progress. Early optimism faded as it became clear that a meaningful improvement in conditions would take longer than anticipated. Housing delivery fell to a historic low, with just 3,248 private housing starts in the first nine months of the year, according to Molior. The emergency measures announced in October were welcome, albeit long overdue.

Expectations for 2026: Land remains a medium-to long-term play, and 2026 could present opportunities for developers willing to take a strategic view. There is an opportunity for forward-thinking developers who can unlock sites now to deliver homes in a few years into a market starved of stock. Early indications suggest more sites will come to market in the first half of the year as landowners anticipate renewed developer appetite. This should support stronger land sales later in the year. If demand-side stimulus is introduced, the next six to twelve months could see a notable uplift in both activity and values.

London New Homes

Year in review: Sales of new homes remained well below historic norms, with just 5,933 transactions recorded between January and September. The uncertainty seen around personal and property taxation ahead of the November Budget will have kept Q4 figures equally as subdued. Indeed, Nationwide and Halifax both reported that annual house price growth approached zero last month, hindered by the endless rumours about which taxes would rise. But despite the more challenging environment, there are still pockets of activity - incentives remain common, as does flexibility on pricing, pointing to competitive conditions for developers.

Expectations for 2026: Expect a two-speed market: resilient demand for well-located, build complete homes, but continued pressure on off-plan sales, particularly in prime central London. Supply shortages should underpin values over the medium term, though transaction volumes are likely to remain below pre-pandemic levels without some form of buy-side support. Financial markets have priced in another rate cut from the Bank of England later this month. Investors now expect 64 basis points of easing by the end of 2026, slightly more than before the Budget, according to Bloomberg analysis. That will enable lenders to keep trimming mortgage rates, which should unleash some pent-up demand and lead to a stronger spring 2026 selling season. Even with this loosening, the market will remain price sensitive - not least because there is more choice than usual. At the end of September, there were roughly 3,400 completed but unsold units in the capital - up from just under 3,000 in 2023 (though still below the 2020 peak). Developers able to demonstrate value through pricing, design, and positioning will be best placed to succeed.

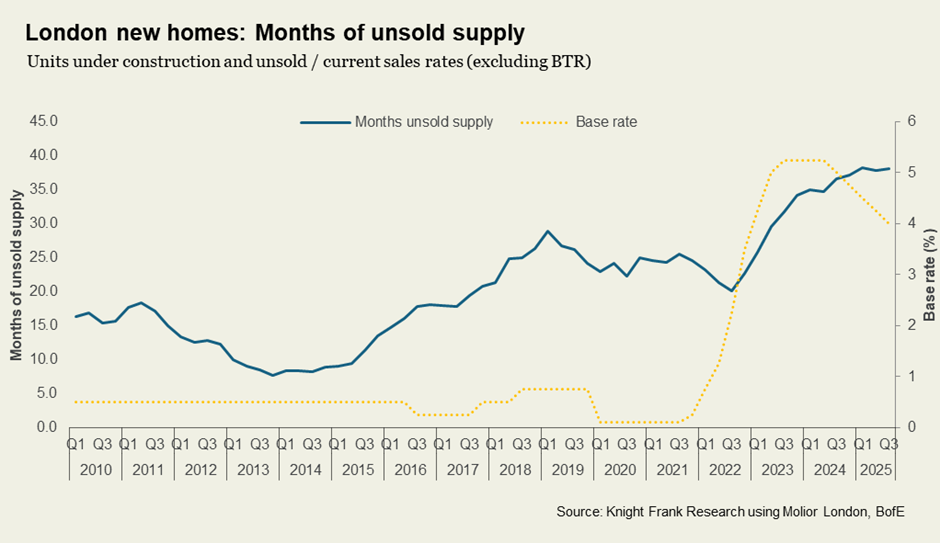

Chart of the Month

The number of unsold homes under construction in London has been falling steadily, from more than 30,000 in 2018 to just over 20,000 today. However, slower sales rates mean this still equates to around 38 months of supply at current sales rates.

Availability will decline as mortgage rates ease from next year, but the figures highlight the significant impact a combination of higher mortgage rates, increased taxation, changes to immigration policy and a lack of government-backed buyer support have had on absorption in the market.

Knight Frank Newcastle

Knight Frank Newcastle is recognised as one of the most progressive and dynamic commercial property estate agent in the region and North East.