UK BTR Market Update Investment Momentum Continues

Posted by Knight Frank Newcastle on 29th October 2025 -

Investment momentum continues

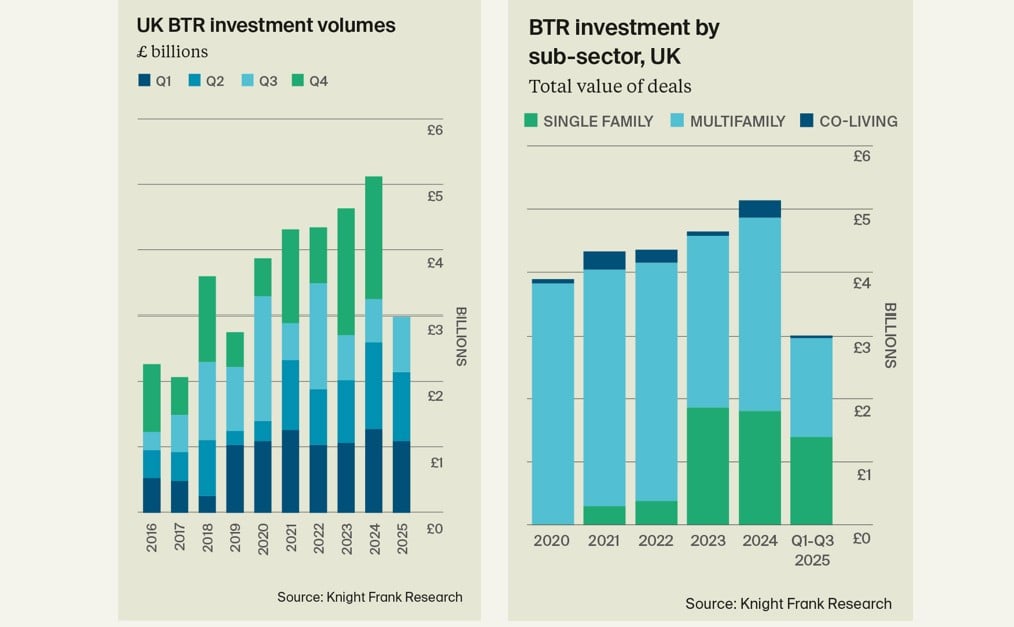

More than £850 million was invested into UK BTR in the third quarter of 2025, up 35% year-on-year. This maintains momentum from the first half of the year, where £2.2 billion was deployed and takes total investment for the first nine months of the year to just over £3 billion across multifamily, single family and co-living deals. Single family continues to perform strongly, accounting for 40% of spend over the course of the quarter and 46% of investment so far this year, reflecting the ongoing strong appetite and liquidity for houses for rent. But more than £500 million was allocated to developing multifamily schemes in urban locations in Q3, suggesting robust demand still for forward funding of large-scale developments.

Volumes v values

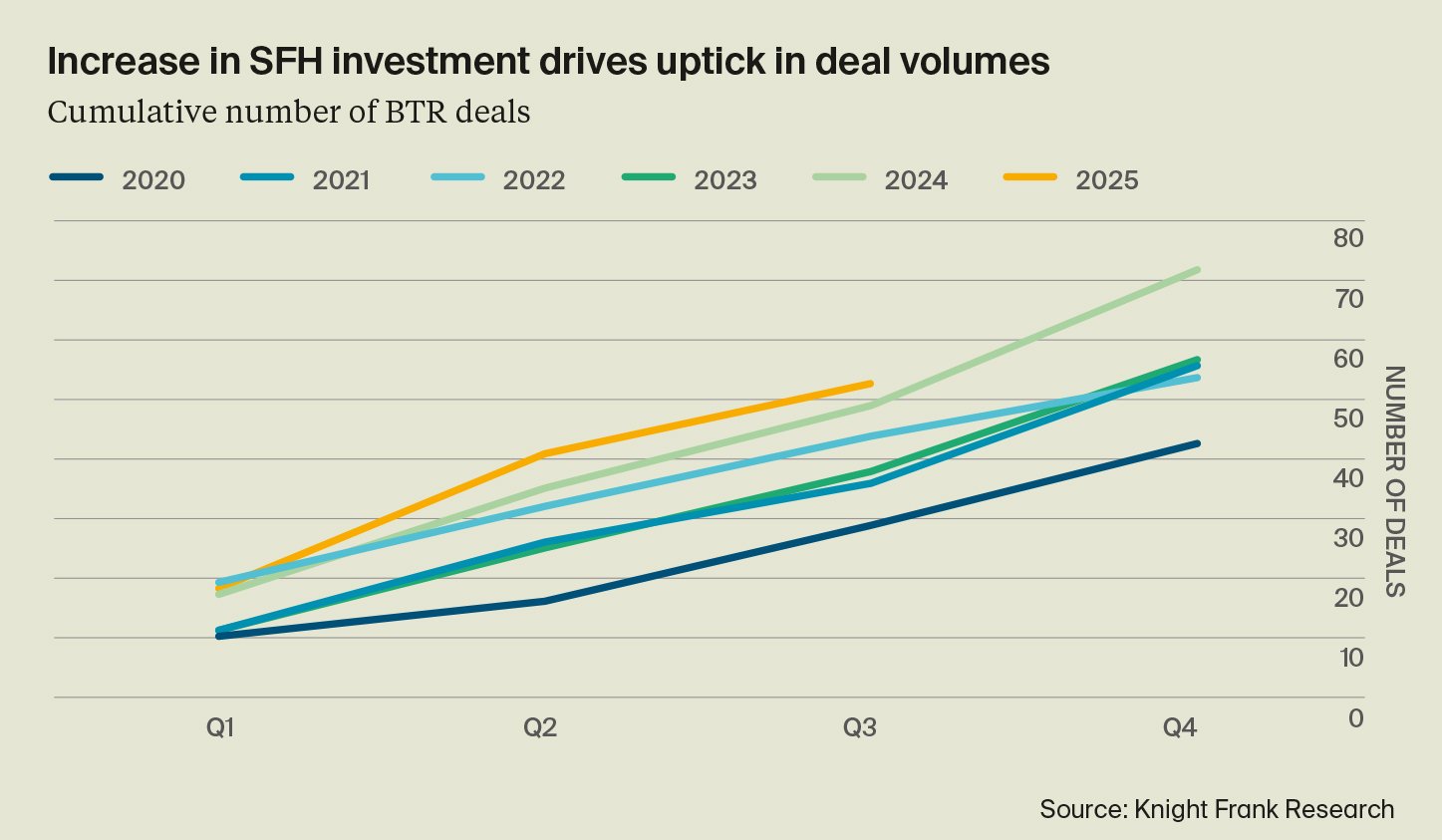

Some 53 deals have completed so far in 2025, up by 8% on the same point last year pointing to an active investment market. Increasing transaction numbers have been supported by the uptick in SFH investment, which tend to be lower lot sizes. Indeed, excluding portfolio deals, the average value of a SFH deal in 2025 so far wasn£42 million, versus £83 million for MFH assets. Persistently high inflation and bond yields are likely to put a dampener on activity for the remainder of the year, as will an element of policy uncertainty in the run-up to the November Budget. However, there is a significant volume of stock under offer or in the market, suggesting it will be a busy run-in to Christmas. Investor appetite remains extremely strong for MFH. Challenges around construction viability, alongside gradually increasing volumes of standing stock have led to an increase in transaction volumes for operational assets. For SFH, transaction volumes remain high across both development deals (where construction viability is less of a challenge than MFH) and operational stock.

‘Not out of the woods yet’

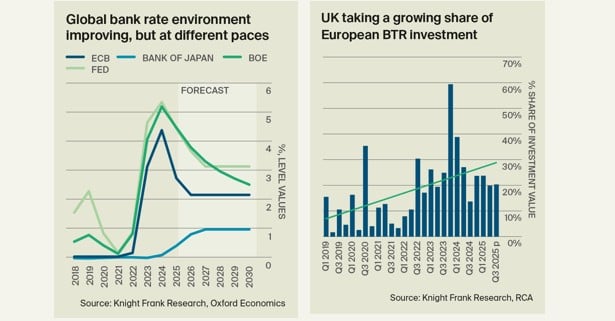

As expected, the Bank of England (BoE) kept interest rates at 4.00% during its September monetary policy committee meeting and announced the decision to dial back its quantitative tightening bond-selling programme from £100 billion to £70 billion. The quantitative tightening target is in line with the BoE’s wider monetary policy plan to effectively reduce the banks’ balance sheet, while ensuring not to impact the government’s wider gilt issuance strategy. Andrew Bailey, the BoE governor, suggested the UK economy was ‘not out of the woods yet’, and while inflation stayed flat in August, unfavourable base rate effects will likely mean inflation will rise in the September reading, and any further rate cuts will need to be made gradually and slowly.

See the wood for the trees

Despite an optimistic view amongst some forecasters that the BoE base rate could fall up to 100bps to 3.00% by the end of 2026, lingering fiscal concerns and a softer economic outlook suggest property yields will stay elevated relative to 10-year government gilts, at least in the medium term. However, the UK is not alone in this scenario, with the spread between long-term government bond yields and property yields a global phenomenon for investors. But investors can see the wood for the trees. For real estate, stable income growth, rather than yield spreads, is what will drive capital growth returns in this cycle. For BTR investors, this means focusing on markets with favourable demand-supply imbalances, and assets with expected value appreciation. Illustrating this is the UK’s growing proportional share of European BTR investment turnover. Despite a more favourable debt landscape in Europe, UK BTR has captured almost 30% of investor appetite across the continent since 2023.

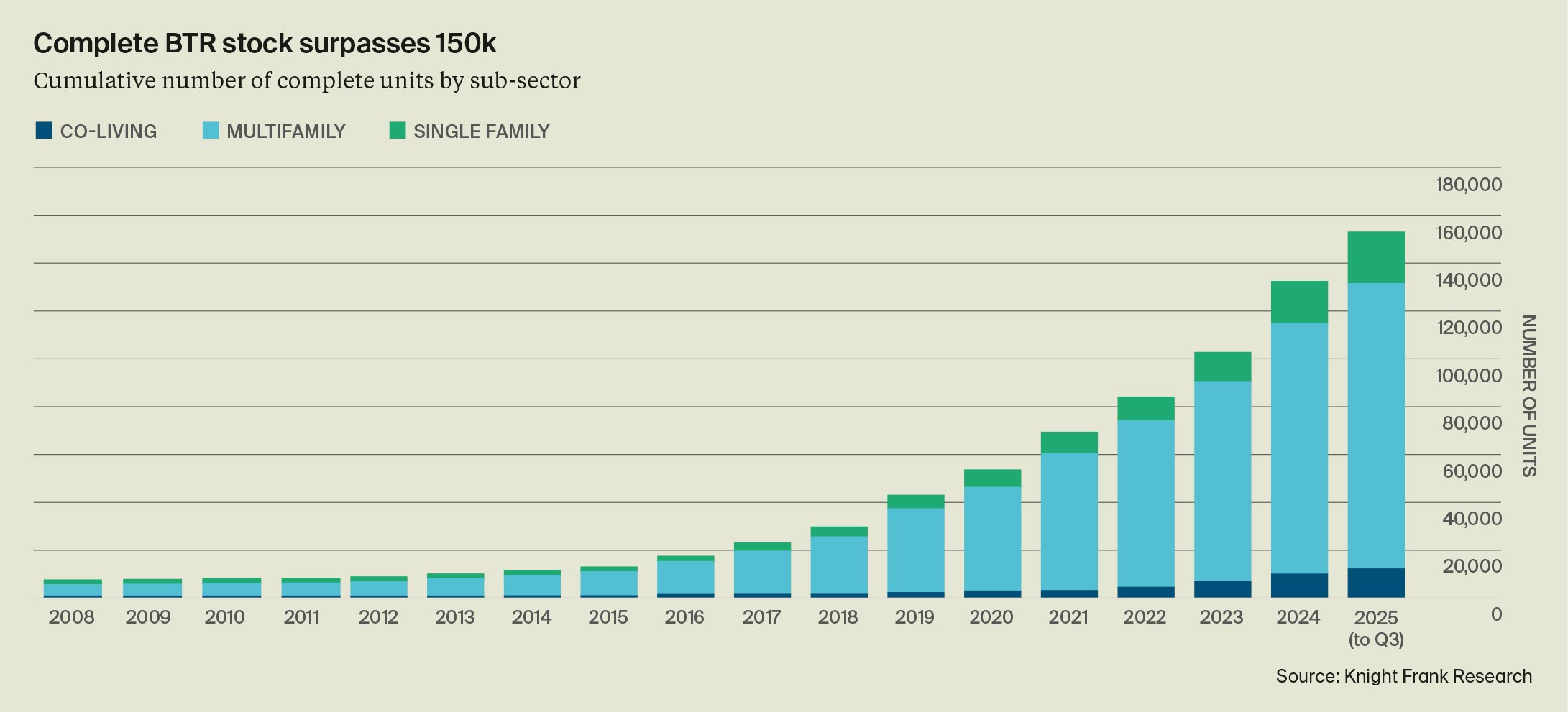

Complete BTR stock surpasses 150k

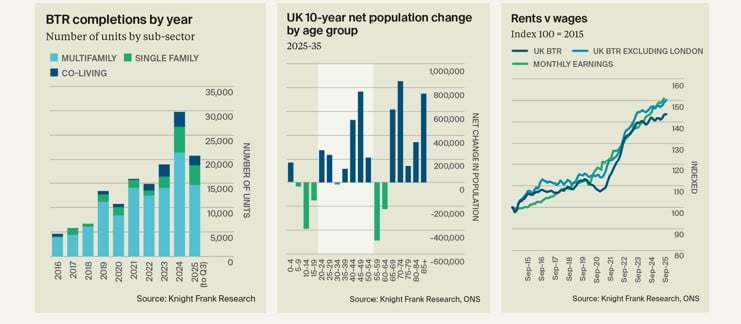

The UK’s BTR stock now stands at 153,367 complete homes, up by 25% compared to Q3 2024. There are a further 54,354 homes under construction meaning the sector should rise to more than 200,000 operational homes within the next few years. That would mark a significant landmark for the sector, yet it remains a fraction of overall demand. Challenges impacting the wider development market, however, mean that outside of the existing development pipeline the longer-term outlook for supply is less certain. So far this year, more than 20,000 BTR homes have completed, putting the sector just behind last year’s record delivery. SFH has accounted for just under a fifth of completions so far this year, up from a tenth in 2021.

Faltering at the start line

As well as the c.207,000 BTR homes built or currently underway, there are a further 111,422 with full planning granted. Turning these into new starts remains a challenge. The number of units under construction is 8% lower than a year ago, suggesting the market is caught up in the wider development slowdown. The result will be falling BTR completions in coming years. Broader market constraints and regulatory hurdles continue to impact the construction sector, especially for high-rise apartments in urban centres. Many developers are unable to start because sites are unviable – hit by high build and finance costs, planning delays, regulatory uncertainty, or exit-route risks – or because schemes over 18 metres are stuck in the Gateway 2 process. The latest official data, released before the government announced reforms to speed up approvals, shows it now takes an average of 36 weeks to secure Gateway approval on new build projects. A lack of clarity on timing of Gateway 3 at the end of construction presents further challenges to viability.

Back in balance?

Rental market conditions are starting to normalise after a frantic few years characterised by many renters chasing too few homes, which supported strong rental growth. Asking rents have risen by 30% since 2020, according to our UK BTR Rental Index. Supply and demand are coming back into balance, with the number of homes listed for rent steadily recovering year-on-year in many locations. In part, this has been supported by growth in BTR supply but also through increased churn in the rental market as first-time buyer numbers slowly increase. However, while there has been a short-term recovery in available supply, the unaffordability of home ownership and expected population growth among 20 to 44-year-olds sitting above long-term averages will keep rental demand for apartments and houses above pre-pandemic levels. In addition, we are continuing to see private BTL landlords (the owners of the majority of rental properties in the UK) leaving the market. As a result, at a time when we desperately need more rental stock, the pool of available properties remains significantly lower than pre-pandemic.

Where next for rents?

Rental inflation remains on track to be 4.0% over 2025, according to Knight Frank forecasts, with an expectation rents across the private rental sector will grow by 18.8% on average over the next five years. An imbalance between supply and demand – likely to deepen considering upcoming policy changes – will be the driving force behind upwards pressure on rents over that time, albeit affordability will act as a moderating force on growth. Rental inflation tends to be anchored by wage growth and, while the recent weakness in the labour market should soon weigh more heavily on pay growth, wages are still expected to average 3.4% in 2026 and 2027, according to Capital Economics.

Delivery and affordability

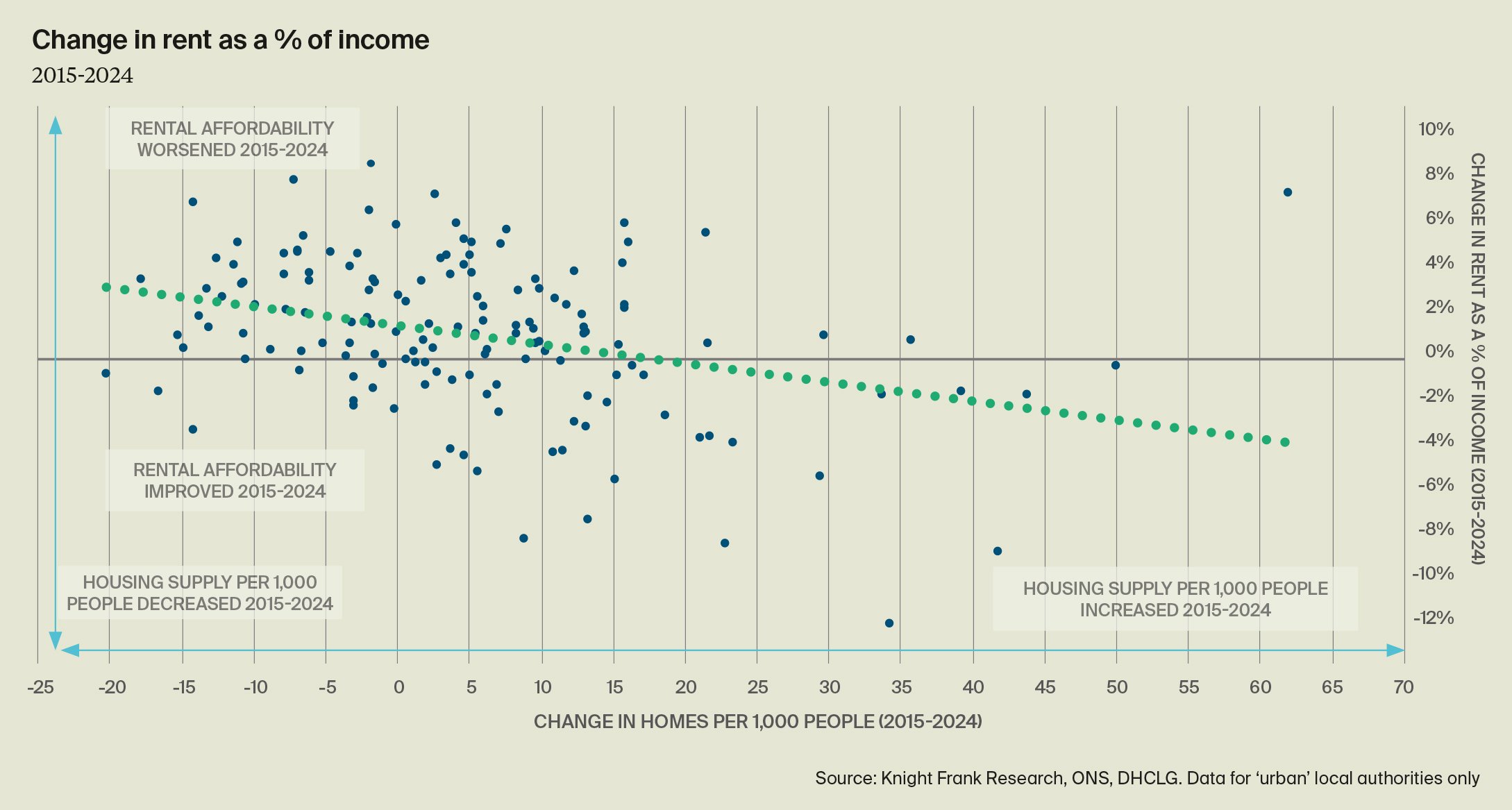

Improving rental affordability depends on increasing housing supply across all tenures. While BTR is making an important contribution, it cannot bridge the gap alone. New investment, policy consistency and a more efficient planning system are all critical to scaling delivery. Our analysis of 149 urban areas across England – tracking changes in housing stock, population, rents, and salaries since 2015 – shows a clear relationship between housebuilding and affordability. Areas that failed to build enough homes to keep pace with population growth have seen affordability worsen, with rents rising faster than wages. In contrast, places that expanded their housing stock more quickly have generally maintained or even improved affordability, as additional supply helped temper growth. The data underscores the central role of housing delivery of any type in improving affordability. Yet the pace of delivery remains well below what’s needed to meet current and future demand. A coordinated effort to streamline planning, de-risk investment, and diversify delivery models – including BTR, build-to-sell, and affordable housing – will be essential to restoring balance and ensuring long-term housing sustainability across the UK.

Read article from Knight Frank

Knight Frank Newcastle

Knight Frank Newcastle is recognised as one of the most progressive and dynamic commercial property estate agent in the region and North East.