Bridge Lending Over Troubled Water: How Financing Type is Keeping Market Safe as Houses

Posted by Whitehall Capital on 14th May 2021 -

The bridge lending market has shown remarkable resilience through Brexit and the ravages of the pandemic. Finance has been readily available to investors and lenders have been active.

However, with valuers pricing on the high side, determining real value has proven a challenge. Bridge lending has nevertheless continued to deliver steady and attractive returns.

Residential to enjoy continuing outperformance

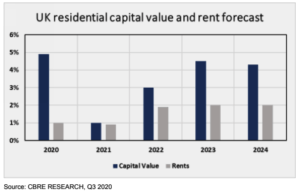

CBRE forecast MSCI UK All Property total returns of -4.4% for 2020, but 2.6% for 2021. Over the next five years, it forecast average returns and rental growth of 4.4% and 0.3% per year respectively, with real estate investment expected to rise by about 30%, from a projected £37bn in 2020 to £48bn in 2021.

Multi-family housing, which represents buildings with multiple dwellings, does not face the same occupier challenges as the more traditional real estate sectors – single-family homes, apartments, condominiums, and planned unit developments – so we expect the trend to continue throughout the year.

CBRE valuation data confirms rent collection and occupancy rates remained robust, averaging 97% and 83% respectively during 2020.

Purpose-built student accommodation, meanwhile, has faced considerable occupational challenges, impacted by widespread outbreaks of Covid-19. Given this issue has largely remedied itself, we anticipate investment in PBSA to build steadily and remain robust.

Residential investment to reach new heights

Regardless of Covid-induced restrictions, residential investment remained strong throughout 2020 – and appetite remains elevated, with a high level of equity targeting the multi-family sector; as much as £40bn according to CBRE.

Lending also remains highly competitive. The emerging co-living sector is seen as attractive given the parallels with the student, build-to rent, hotels and co-working sectors – all of which have experienced exponential growth in the past five-to-ten years.

They are expected to gain further traction in 2021, with investors continuing to target opportunities in PBSA.

Given its resilience and strong long-term fundamentals, we expect residential investment to break records almost every year through 2025, with existing investors expanding their portfolios and new entrants diversifying from traditional commercial real estate.

Debt in the UK

UK households entered the pandemic in a stronger financial position than they did the Global Financial Crisis. According to the Bank of England’s Financial Stability Report (August 2020), household debt (excluding student loans) in Q1 2020 equated to 123% of total household income – high by historic standards, but lower than the 2008 peak of 144%.

Government- and bank-led support, especially payment holidays, furlough and limits on high LTV mortgages, have kept consumer credit under control, so far – but this may change, and quickly, if unemployment rises faster than policymakers expect.

Powered by a surge of pent-up demand, residential sales rebounded sharply in the wake of the initial lockdown, with the UK Government’s Stamp Duty Land Tax holiday delivering further support.

This, according to Bank of England data, contributed to a 22% increase in mortgage approvals in Q3 2020, compared with Q3 2019.

The Nationwide, however, reports that England was the weakest performing home nation in the three months to March 2021, with annual house price growth of 6.4% – a slight slowing on Q4 2020, when prices rose at an annual rate of 6.9%.

While policy support is likely to boost the market over the coming six months, the longer-term outlook remains uncertain.

This momentum will continue through the year, with a surge of sales likely during the extended SDLT holiday; revisions to the Help to Buy scheme take effect from April and should power movement further up the ladder.

The biggest influence on the performance of the housing market will be the broader economic backdrop. Even with a rebound, weaker GDP growth and higher unemployment will feed through, with negative impacts likely to be in evidence.

We see house prices and rents remaining broadly stable in 2021, increasing by 1% and 0.9% respectively. Bridge finance will certainly play an important role in stimulating the market, allowing a swift completion of deals and helping to move the economic recovery forward.

Anthony Bodenstein – founder and managing partner of Whitehall Capital Management

Whitehall Capital

We are a specialist provider of bridge, short-term, auction and development finance solutions – 100% privately funded, with more than a decade in the market.